{kind=link}

Adobe simply paid $1.9 billion for Semrush. Not for the LLM monitoring dashboards. For the platform, the client relationships, and the distribution.

Distinction: Traders poured $227 million into AI visibility monitoring. Most of that went to monitoring dashboards. The businesses delivery outputs from agentic web optimization raised a 3rd of that. Adobe’s acquisition proves dashboards had been by no means the purpose.

Traders chased LLM monitoring as a result of it appeared like simple SaaS, however the sturdy worth sits in agentic web optimization instruments that truly ship work. Why? As a result of agentic web optimization goes past the normal web optimization tooling setup, and provides web optimization professionals and businesses a very new operational functionality that may increase (or doom) their enterprise.

Along with Wordlift, Development Capital, Niccolo Sanarico, Primo Capital, and G2, I analyzed the funding knowledge and the businesses behind it. The sample is obvious: Capital chased what sounded progressive. The actual alternative hid in what really works.

1. AI Visibility Monitoring Seemed Like The Future

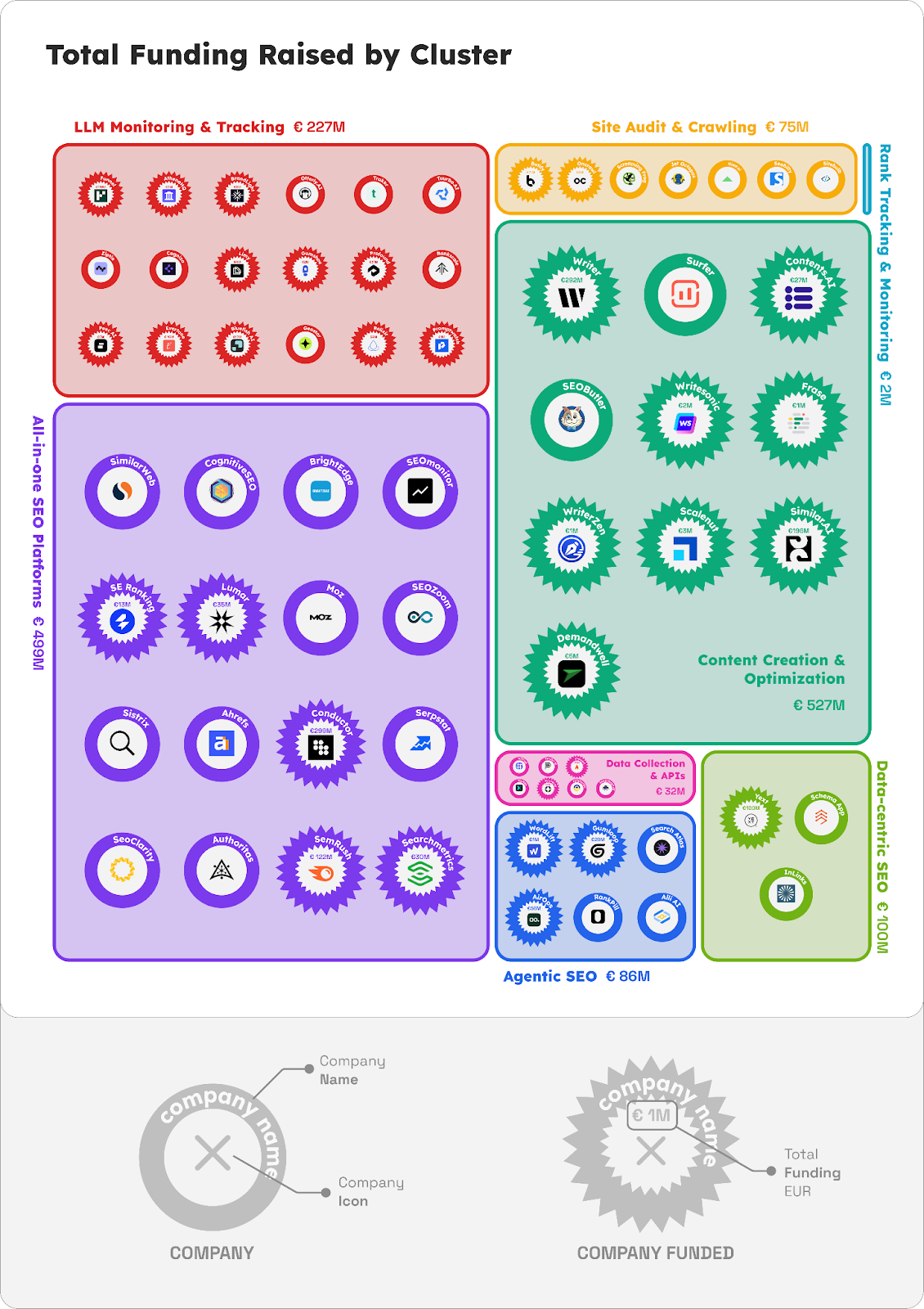

We checked out 80 corporations and their collective $1.5 billion in enterprise funding:

- Established platforms (5 corporations) captured $550 million.

- LLM Monitoring (18 corporations) cut up $227 million.

- Agentic web optimization corporations bought $86 million.

AI visibility monitoring appeared like the apparent drawback in 2024 as a result of each CMO requested the identical query: “How does my model present up in ChatGPT?” It’s nonetheless not a solved drawback: We don’t have actual consumer prompts, and responses range considerably. However measuring isn’t defensible. The huge variety of startups offering the identical product proves it.

Monitoring instruments have unfavourable switching prices. Agentic instruments have excessive switching prices.

- Low ache: If a model turns off a monitoring dashboard, they lose historic charts.

- Excessive ache: If a model turns off an agentic web optimization platform, their advertising and marketing stops publishing.

Enterprise capital collectively invested +$200 million as a result of corporations care about how and the place they present up on the primary new channel since Alphabet, Meta, and TikTok. The AI visibility trade has the potential to be larger than the web optimization trade (~$75 billion) as a result of Model and Product Advertising and marketing departments care about AI visibility as nicely.

What they missed is how briskly that pattern turns into infrastructure. Amplitude proved it was commoditizable by providing monitoring totally free. When Semrush added it as a checkbox, the class collapsed.

2. The Alpha Is In Outcomes, Not Insights

Outcomes trump insights. In 2025, the worth of AI is getting issues performed. Monitoring is desk stakes.

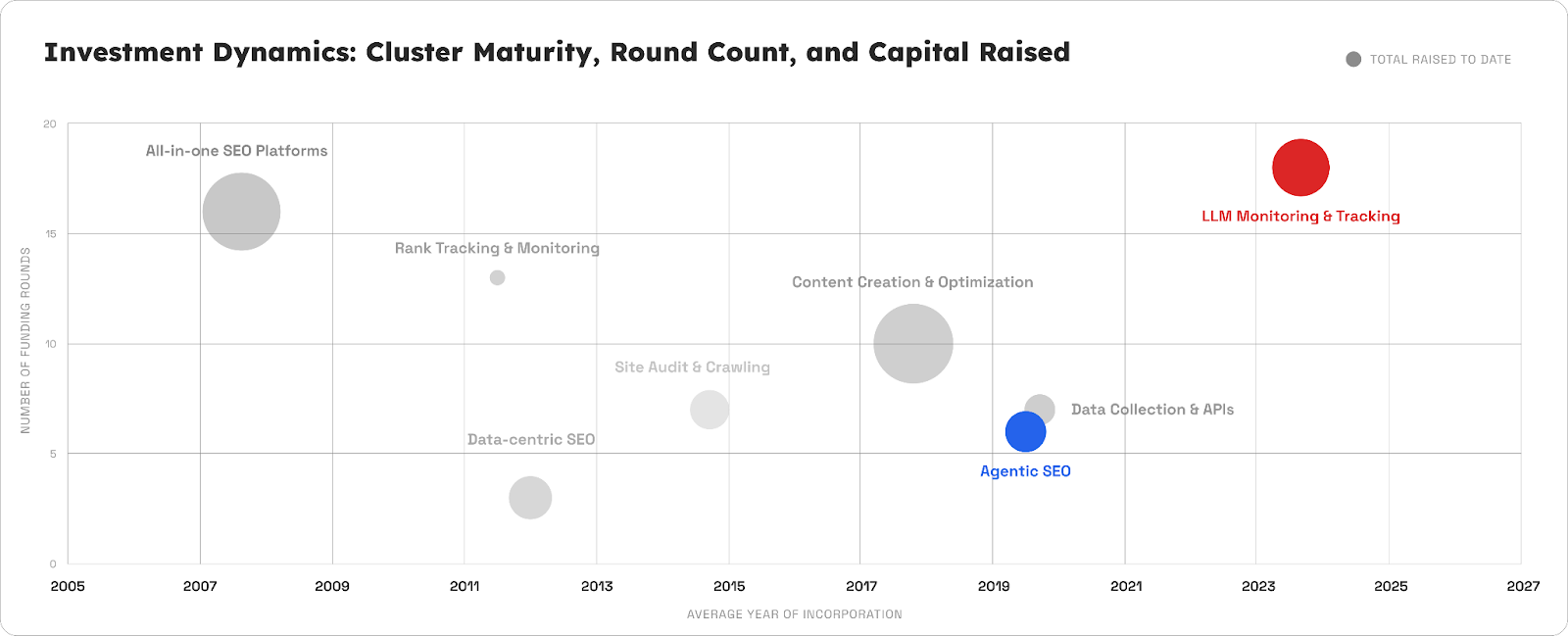

73% of AI visibility monitoring corporations had been based in 2024 and raised $12 million on common. That test dimension is often reserved for scale-stage corporations with confirmed market-fit.

Our evaluation reveals a large maturity hole between the place capital flowed and the place worth lives.

- Monitoring corporations (common age: 1.3 years) raised seed capital at development valuations.

- Agentic web optimization corporations (common age: 5.5 years) have been constructing infrastructure for practically a decade.

Regardless of being extra mature, the agentic layer raised one-third as a lot capital because the monitoring layer. Why? As a result of buyers missed the moat.

Traders dislike “delivery” instruments on the seed stage as a result of they require integration, approval workflows, and “human-in-the-loop” setup. To a VC, this seems to be like low-margin consulting. Monitoring instruments appear to be excellent SaaS: 90% gross margins, instantaneous onboarding, and 0 friction.

Cash optimized for ease of adoption and missed ease of cancellation.

- The Monitoring Lure: You possibly can flip off a dashboard with a click on to avoid wasting finances.

- The Execution Moat: The “messy” friction of agentic web optimization is definitely the defensibility. As soon as an operational workflow is put in, it turns into infrastructure. You can not flip off an execution engine with out halting your income.

Capital flowed to the “clear” financials of monitoring, leaving the “messy” however sturdy execution layer underfunded. That’s the place the chance sits.

Three capabilities separate the winners from the options:

- Execution Velocity: Manufacturers want content material shipped throughout Reddit, TikTok, Quora, and conventional search concurrently. Winners automate the whole workflow from perception to publication.

- Grounding in Context: Generic optimization loses to methods that perceive your particular enterprise logic and model voice. (Ontology is the brand new moat).

- Operations at Scale: Content material era with out pipeline administration is a toy. You want methods implementing governance throughout dozens of channels. Level options lose; platform performs win.

The distinction is easy: one group solves “how do I do know?” and the opposite solves “how do I ship?”

3. The Subsequent 18 Months Will Wipe Out The Weakest Half Of The AI Stack

The market types into three tiers based mostly on defensibility:

1. Established platforms win by commoditizing. Semrush and Ahrefs have buyer relationships spanning 20 years. They’ve already added LLM monitoring as a characteristic. They now want to maneuver sooner on the motion layer – the workflow automation that helps entrepreneurs create and distribute property at scale. Their danger isn’t dropping relevance. It’s shifting too slowly whereas specialised startups show out what’s potential.

The problem: Established platforms are read-optimized; agentic operations require write-access. Semrush and Ahrefs constructed 20-year moats on indexing the net (Learn-Solely). Shifting to agentic web optimization requires them to put in writing again to the client’s CMS (Write-Entry).

2. Agentic web optimization platforms scale into the hole. They’re fixing actual operational constraints with sticky merchandise. AirOps is proving the thesis: $40 million Collection B, $225 million valuation. Their product lives within the motion layer – content material era, upkeep, wealthy media automation. Underfunded at this time, they seize follow-on capital tomorrow.

3. Monitoring instruments consolidate or disappear. Standalone AI visibility distributors have 18 months to both construct execution layers on high of their dashboards or discover an acquirer. The market doesn’t assist single-function monitoring at enterprise scale.

Q3/This fall 2026 may very well be an “Extinction Occasion.” That is when the 18-month runway from the early 2024 hype cycle runs out. Firms will go to market to boost extra money, fail to point out the income development required to assist their 2024 valuations, and be pressured to:

- Settle for a “down-round” (elevating cash at a decrease valuation, crushing worker fairness).

- Promote for elements (acqui-hire).

- Fold.

Let’s do some fundamental “Runway Math”:

- Assumption: The dataset reveals the typical “Final Funding Date” for this cluster is March 2025. This implies the majority of this €227 million hit financial institution accounts in Q1 2025.

- Information Level: The common firm raised ~€21 million.

- The Calculation: A typical Collection A/Seed spherical is calculated to offer 18 to 24 months of runway. With the final funding in Q1 2025 and 18 months of runway, we arrive at Q3 2026.

To boost their subsequent spherical (Collection B) and lengthen their life, AI visibility corporations should justify the excessive valuation of their earlier spherical. However to justify a Collection A valuation (seemingly $50-$100 million post-money given the AI hype), they should present roughly 3x-5x ARR development year-over-year. As a result of the product is commoditized by free instruments like Amplitude and bundled options from Semrush, they may miss that 5x income development goal.

Andrea Volpini, Founder and CEO of Wordlift:

After 25 years, the Semantic Internet has lastly arrived. The concept that brokers can attain a shared understanding by exchanging ontologies and even bootstrap new reasoning capabilities is not theoretical. It’s how the human-centered net is popping into an agentic, reasoning net whereas many of the trade is caught off guard. When Sir Tim Berners-Lee warns that LLMs might find yourself consuming the net as a substitute of people, he’s signaling a seismic shift. It’s larger than AI Search. It’s reshaping the enterprise mannequin that has powered the net for 3 many years. This AI Map is supposed to point out who’s laying the foundations of the reasoning net and who’s about to be left behind.

4. The Market Thesis: When $166 Billion Meets Behavioral Disruption

From Niccolo Sanarico, author of The Week in Italian Startups and Companion at Primo Capital:

Let’s go away the funding knowledge for a second, and shift to the demand aspect of the market: on the one hand, Google integrating AI search outcomes on its SERP, ChatGPT or Perplexity changing into the entry level for search and discovery, are phenomena which are making a change in consumer conduct – and when customers change conduct, new giants emerge. However, web optimization has traditionally been a consulting-like, human-driven, tool-enabled effort, however its elements (knowledge monitoring & evaluation, content material ideation & creation, course of automation) are the bread and butter of the present era of AI, and we imagine there’s a big area for rising AI platforms to chip away on the consulting aspect of this enterprise. Unsurprisingly, 42% of the businesses in our dataset had been based on or after 2020, regardless of the oldest and best gamers courting again greater than 20 years, and the important thing message they’re passing is “allow us to do the work.”

The numbers validate this thesis at scale. Despite the fact that it isn’t all the time simple to dimension it, current analysis finds that the web optimization market represents a $166 billion alternative cut up between instruments ($84.94 billion) and companies ($81.46 billion), rising at 13%+ yearly. However the distribution reveals the disruption alternative: businesses dominate with 55% market share in companies, whereas 60% of enterprise spend flows to massive consulting relationships. This $50+ billion consulting layer – constructed on guide processes, relationship-dependent experience, and human-intensive workflows – sits straight in AI’s disruption path.

The workforce knowledge tells the automation story. With >200,000 web optimization professionals globally and median salaries within the US of $82,000 (15% above U.S. nationwide common), we’re a information employee class ripe for productiveness transformation. The job market shifts already sign this transition: content-focused web optimization roles declined 28% in 2024 as AI automation eradicated routine work, whereas management positions grew 50-58% as the main focus shifted to technique and execution oversight. When 90% of latest web optimization positions come from corporations with 250+ staff, and these organizations are concurrently rising AI software budgets from 5% to fifteen% of complete web optimization spend, the trail ahead is obvious: AI platforms that may ship execution velocity will seize the worth hole between high-cost consulting and lower-margin monitoring instruments.

5. What This Means For You

For Device Consumers

Cease asking “Is it AI-powered?” Ask as a substitute:

- Does this remedy an operational constraint or simply give me data? (If it’s data, Semrush may have it free in 18 months.)

- Does this automate a workflow or create new guide work? (Sticky merchandise are deeply built-in. Level options require babysitting.)

- Can I get this from my current platform ultimately, or is that this defensible? (If a longtime participant can bundle it, they’ll.)

For Traders

You’re at an inflection level:

- The narrative layer (monitoring) is collapsing in real-time.

- The substance layer (execution) remains to be underfunded.

- This hole closes quick.

When evaluating alternatives, ask: “What would want to occur for Semrush or Ahrefs to offer this?” If the reply is “not a lot,” it’s not defensible at enterprise scale. In the event that they needed to rebuild core infrastructure or cannibalize a part of their product, you might have a moat.

One of the best sign isn’t which corporations are elevating capital, however which classes are elevating capital regardless of low defensibility. That’s the place you discover the upside.

For Builders

Your strategic query isn’t “Which class ought to I enter?” It’s “How deeply built-in will I be in my clients’ workflows?” When you’re constructing monitoring instruments, you might have 18 months. Both construct an execution layer on high of your dashboard or optimize for acquisition.

When you’re constructing execution platforms, defensibility comes from three issues:

- Depth of integration in day by day workflows

- Required area experience

- Operational leverage you present relative to constructing in-house

The profitable corporations are those who remedy issues needing steady area experience and can’t be simply copied. Automated workflows that perceive model tips, buyer segments, and channel-specific finest practices aren’t.

Ask your self: What operational constraint am I fixing that requires judgment calls, not simply higher AI? If the reply is “I’m simply producing higher content material sooner,” you’re constructing a characteristic. If the reply is “I’m managing complexity throughout dozens of channels whereas implementing consistency,” you’re constructing a platform.

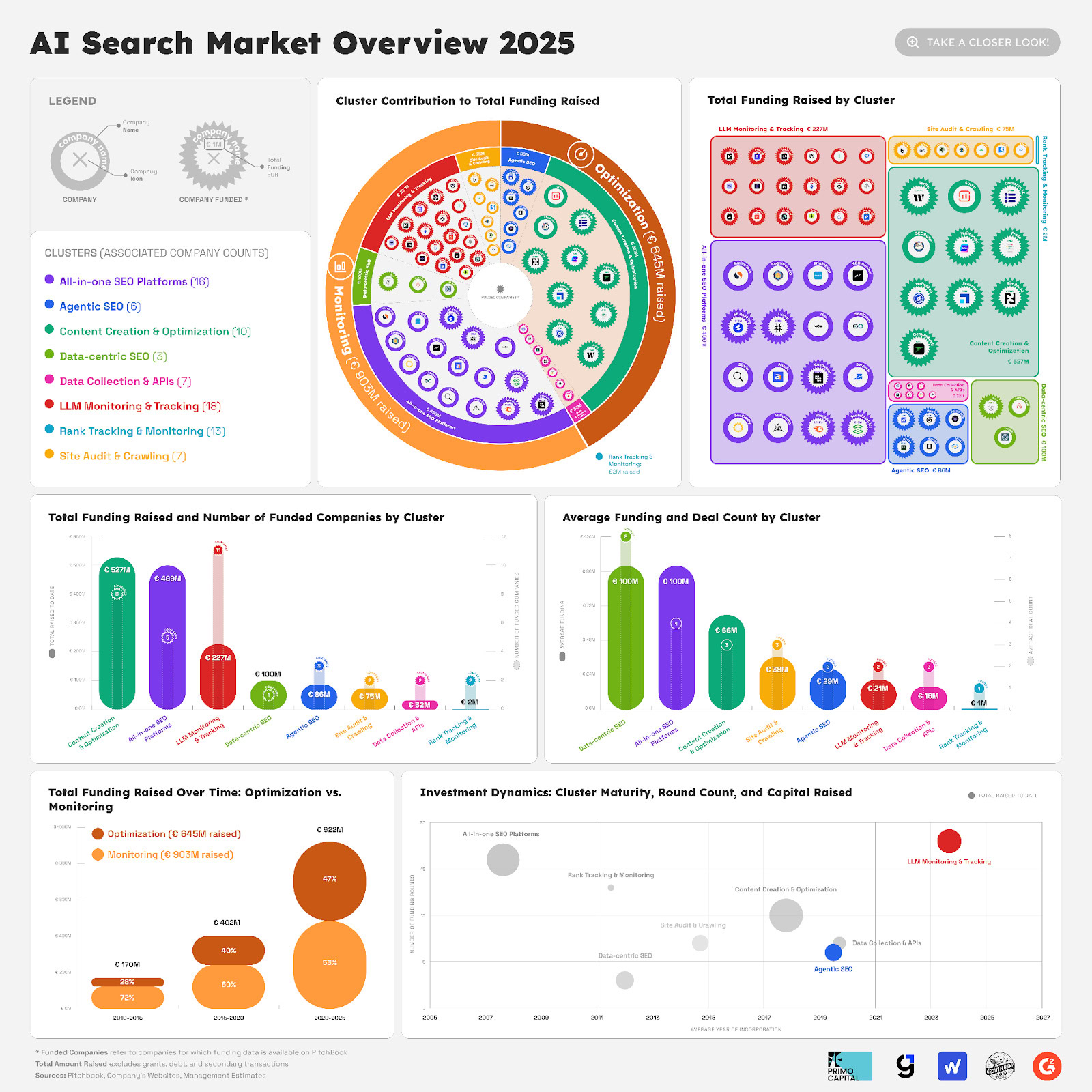

Full infographic of our evaluation:

Enhance your expertise with Development Memo’s weekly skilled insights. Subscribe totally free!

Featured Picture: Paulo Bobita/Search Engine Journal